Our industry is changing at an unprecedented rate. Health systems must examine new ways of doing business in order to succeed in the years ahead. But how can health systems compete as consolidation, payer mix shifts, and vertical integration continue to disrupt the market?

The shift from volume- to value-based care and the need to better manage the health of populations have challenged health systems to deliver better care at lower costs. As a means to achieve those goals and stay relevant in a rapidly changing healthcare landscape, many are entering the insurance business.

Becoming an insurer appeals to providers for a number of reasons. It gives them more control over the premium dollar from beginning to end. Health systems also see operating an insurance plan as a way to gain more patients and the associated revenue at a time when inpatient volume is declining. Finally, they see promising business opportunities in certain lines of health insurance, such as Medicare Advantage.

However, while moving into insurance operations can have financial and quality advantages, it is not without challenges.

Roadblocks to Success

Getting into insurance product design and pricing are areas that fall outside the expertise of most health systems. And once established, health plan success doesn’t happen overnight. Plans also need to be cautious of attracting too many sicker members.

Take Partners HealthCare, for example. The health system acquired Neighborhood Health Plan four years ago to move into the insurance business and reach a broader population of patients. It hoped it could develop better ways of delivering care to patients with complex illnesses. After posting an operating loss of $108 million in 2016, $104 million of which was attributable to Neighborhood, it is under pressure to get the insurer back on solid financial ground. According to Partners, the losses are attributable to higher pharmaceutical and medical claims costs associated with the state’s Medicaid program, MassHealth, and low reimbursement rates from the state.

Financial conditions improved in 2017 with a net operating gain of $46 million. The growth is attributable to expanding its commercial business while not accepting new Medicaid members.[1] To operate a health plan, providers must understand their core capabilities and admit that operational deficiencies may lead to prolonged challenges.

What Level of Risk Will You Assume?

Health systems have many options for moving into insurance operations, including building a health plan, entering into a joint venture with a payer and establishing an accountable care organization. The decision is often dictated by how much risk a provider is willing to assume. Regardless of the model chosen, providers considering getting into the insurance business must be willing to deal with many complex government requirements, such as maintaining significant reserves and paying the ACA’s health insurance tax.

The potential for conflicts with other insurers in their market is another consideration for health systems. To avoid competing with other insurers, many opt to pursue small-scale startups. Medicare Advantage is attractive to many providers because they feel well equipped to manage seniors’ care.

Medicare’s Pioneer and Shared Savings ACOs are giving providers the experience to manage risk, making fully capitated Medicare Advantage a logical next step. Without first investing in insurance expertise, infrastructure and information technology needed to succeed in the health plan business, however, even starting a Medicare Advantage plan isn’t a guaranteed path to success.

For example, a provider-sponsored Medicare Advantage plan in the southeast launched in 2014 to capitalize on the local market opportunity. At that time, about 31.2 percent of seniors in the area were in a Medicare Advantage health plan, suggesting room for further growth.

However, the new health plan closed two years later, after enrolling 15,352 members, mostly seniors. It lost $11.4 million in 2014 and $24.4 million in 2015. The health plan told providers it was leaving the Medicare business because it was unable to generate a large enough membership and the required premium revenues needed for long-term operations and sustainability. It also said it was expensive to comply with Medicare Advantage rules, especially when operating with a relatively small number of enrollees. [2]

Taking the Long View

The journey to positive margins doesn’t happen overnight. Most experts agree that hospital-owned plans need to have several hundred thousand covered lives before finances become sustainable. That means profitability can be several years down the road. How can providers ensure a viable strategy?

Healthcare providers that lack experience in value-based care must expand their capacity to manage the health of populations. Providers should examine their goals, core capabilities, market situation and market potential, as well as their organizational and financial status when making the move into payer operations.

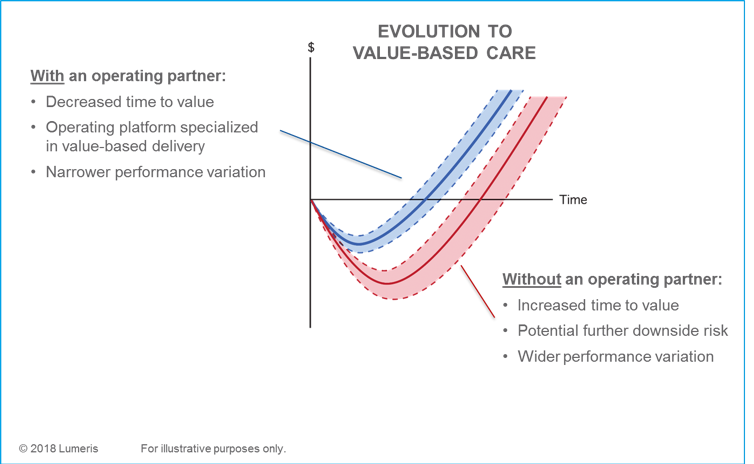

For many health systems, success begins by working with an operating partner or a traditional insurer rather than building and operating their own plan. An operating partner with a proven track record supports provider systems with plan administrative services, provider and care team engagement, and actionable data for population health management. This creates a faster route to success, and is a key strategy for remaining relevant in today’s value-based care environment. Are you ready to begin the journey?

[1] “Partners HealthCare turns around worst financial loss to a profit in 2017,” Becker’s Hospital Review, Dec. 8, 2017.

[2] Andy Miller, “Hospitals retreat from insurance venture,” Atlanta Journal Constitution online content, Sept. 25, 2015